Investment Scams

Be suspicious of anyone that offers you easy money. Scammers are skilled at convincing you that the

Behavioral scientist Abraham Maslow wrote “A Theory of Human Motivation” in 1943, arguing that humans worldwide are influenced by a “hierarchy of needs”.

This theory organizes human needs across five levels, where needs in the lower end must be satisfied before progressing onto the next level. At one end are physiological needs such as sleep and shelter, while at the other end are esteem and self-actualisation. This Markets in a Minute chart from New York Life Investments explores how Maslow’s theory applies to our financial needs, pinning down the steps to creating a strong financial foundation.

The Essentials

What are the five levels in the hierarchy of financial needs?

1. Cash flow and basic needs:

Covering food, housing and daily expenses. Ensuring the fundamentals, including our physiological needs, are covered financially.

2. Financial safety:

This covers insurance and an emergency fund to help prepare for unforeseen events and risks. As a safety cushion, an emergency fund should cover three months of living expenses in case of an accident, an unexpected health or family issue, or losing a job.

3. Accumulating wealth:

This includes growing investments, paying down debt, and saving for retirement. At this level, the focus shifts to growing assets for long-term success and longevity.

4. Financial freedom:

Long-term care and children’s education are found within this category, along with retirement savings and vacations. These financial needs are linked with esteem needs, such as self-respect and personal accomplishment.

5. Legacy:

Estate planning, tax planning, and business succession planning all fall within this category, connecting with self-actualization in Maslow’s pyramid.

Naturally, financial needs can shift based on a given situation. But as a general rule of thumb, moving along this path can help create an enduring roadmap for financial health.

Financial Needs Under the Microscope

While it’s easy enough to describe the theory in concept, how does the hierarchy of financial needs impact our day-to-day lives in practice?

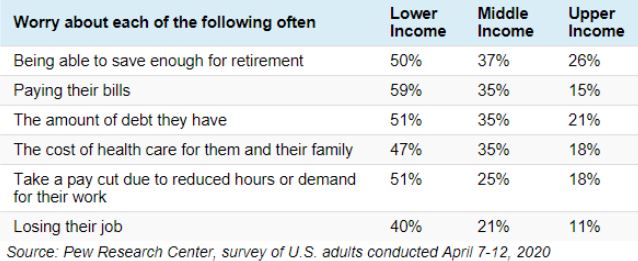

To start, as individuals live longer, many are concerned with having enough savings for retirement—across all income levels.

For Americans in the lower income bracket, 50% worry about their retirement savings, while 26% worry in upper income levels.

Debt is also a primary concern among many Americans, as the cost of both healthcare and education have continued to rise. Average annual college costs, for example, have risen 25% over the last

decade, while U.S. household debt has roughly doubled to $14 trillion since 2004. It’s only once these above needs are taken care of that individuals can focus on the top of the financial needs hierarchy, taking care of legacy-focused items such as estate and tax planning, or business succession planning.

The Importance of Wealth Management

To navigate the hierarchy of financial needs, the importance of having a robust financial plan comes into focus. Especially during times of uncertainty, individuals need a framework that accounts

for changing life circumstances, such as a new job or purchasing a house. And when individuals move up each rung of the financial needs pyramid, they must also recognize how their tactics might need to change to best pursue their financial goals. Cultivating a stronger awareness of financial needs can help individuals make more informed choices, on both a micro and macro level—from day-to-day purchases to long-term investment decisions.

Be suspicious of anyone that offers you easy money. Scammers are skilled at convincing you that the

Easy steps to plan and manage how you spend your money. Having a budget helps you to feel in

When we get to the end of another year, we often feel the stress and events of the last 12 months

Level 1, 441 South Road Bentleigh VIC 3204